Many of us have numerous credit cards, but what role do they play in our credit score? They are useful tools in many ways. Credit cards can be used to help us pay for things instead of having to carry cash with us, big purchases, or in emergencies. The key to using credit cards is they must be used responsibly to build your credit. Otherwise, they can hurt your credit score.

The credit limit and the amount of credit that is used on the credit card is called credit utilization. Your credit utilization is worth 30% of your FICO score and up to 192.5 points. It has a massive impact on your credit score.

Credit Utilization – What is it?

Credit utilization is the amount of available credit that is being used. If your credit utilization is low, it is raising your credit score. By only using a small portion of the credit available, it shows that credit is being used responsibly and is seen as a positive indication of responsible credit usage.

The credit utilization rate is calculated using revolving credit. Credit cards are examples of revolving credit. This type of credit does not have an end date, and the amount owed per month fluctuates according to the amount charged. It is not a fixed amount every month. Credit accounts that are not used to calculate utilization are categorized as installment credit. Examples of installment credit are home and car loans. Installment credit has a set end date and a specific amount every month until the obligation is paid in full.

To calculate credit utilization, divide the credit limit of the credit card by the balance on the credit card.

Credit Utilization Examples

Bad Example – Capital One Visa has a $1,000 credit limit, and $900 has been charged on the card. The utilization of this card is 90% and is hurting the credit score.

Good Example – Capital One Visa has a $1,000 credit limit, and $290 has been used on the card. The utilization on this card is 29% and is boosting the score because the usage is below 30%

Best Example – Capital One Visa has a $1,000 credit limit, and $20 has been used on the card. The utilization on this card is 2% and is provide a more significant boost to the credit score.

Credit Utilization and How it Affects a Credit Score

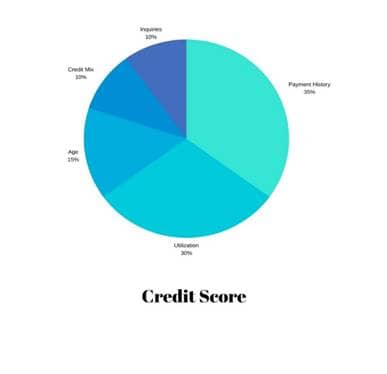

A FICO (Fair Issac Corporation) credit score ranges from 300 to 850. There are 5 parts to a FICO score.

Payment history – 35% of the credit score

Credit utilization – 30% of the credit score

Age of credit – 15% of the credit score

Mix of credit – 10% of the credit score

New credit inquiries – 10% of the credit score

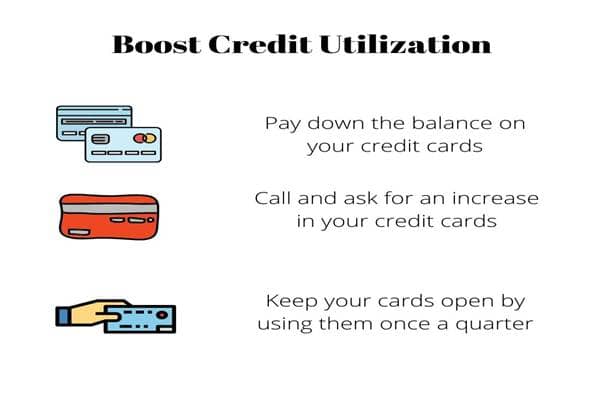

Ways to Improve Credit Utilization

It is vital to do everything possible to increase a low credit score. A low credit score can hurt you and cause credit denial, higher interest rates, higher insurance rates, and not being able to qualify for certain types of employment. A quick way to improve a poor credit score is to lower credit utilization.

- Pay Down the Balance on Your Credit Cards

One of the most important steps you can take in improving your credit score is paying down your credit cards. Come up with a plan on how much extra you can pay off every month. Start with the smallest balance card and work your way up to the card with the highest balance. If you stick to this plan, your credit score will improve.

Another option, if your credit is good, is to apply for a personal loan with low-interest rates. You could use the loan to pay off all your high-interest credit cards. This would allow you to pay less money on interest and more money towards the balance. If you do take this option, you must be very disciplined and use all the available credit you now have on the credit cards. This would not help your credit score.

- Call and Ask for an Increase on Credit Cards

Getting an increase in the credit limit of a credit card will improve the utilization ratio of that account. As an example, a credit card with a $1,000 credit limit and $900 has 90% utilization, but if the credit card limit is raised to $5,000, the utilization drops to 18%. The drop in the utilization rate will improve the credit score fast.

The only downside is when a credit increase is requested, and it causes a hard pull, also known as an inquiry on the credit report. A hard inquiry can cause your credit score to drop slightly. Only use this strategy if all your accounts are in good standing with no recent late payments. If your accounts are not the credit increase will not be given, and you will have an inquiry on your credit report. The credit card increase request will cause your score to drop, and the situation will be worse than it was.

A good rule to follow before asking for a credit increase is to order a copy of your free annual report at annualcreditreport.com. The credit reports from annualcreditreport.com do not provide a score but give the details on each account reporting on Experian, TransUnion, and Equifax. This will allow you to review all your reporting accounts. Make sure that all the information is correct, belongs to you, and has no recent late payments before requesting a credit increase.

- Keep Your Cards Open

If you have paid your credit cards down to zero, you may think about closing them so that you never have to worry about paying down that debt again. DON’T DO IT! Closing accounts will hurt your score.

Its also really important to use your credit card accounts. Sometimes creditors will close accounts that have no activity. Do not let that happen. Use them once a quarter for a small item and pay them off.

If you still have questions about your credit, give us a call. We are credit score improvement specialists. Give us a call and see how we can help you improve your credit score (360) 312-7164.